1. Understanding the Deduction Limits

The IRS treats cryptocurrency as property, not currency, for tax purposes. As a result, donations of appreciated cryptocurrency are generally subject to the same charitable deduction rules that apply to stocks and other capital assets.

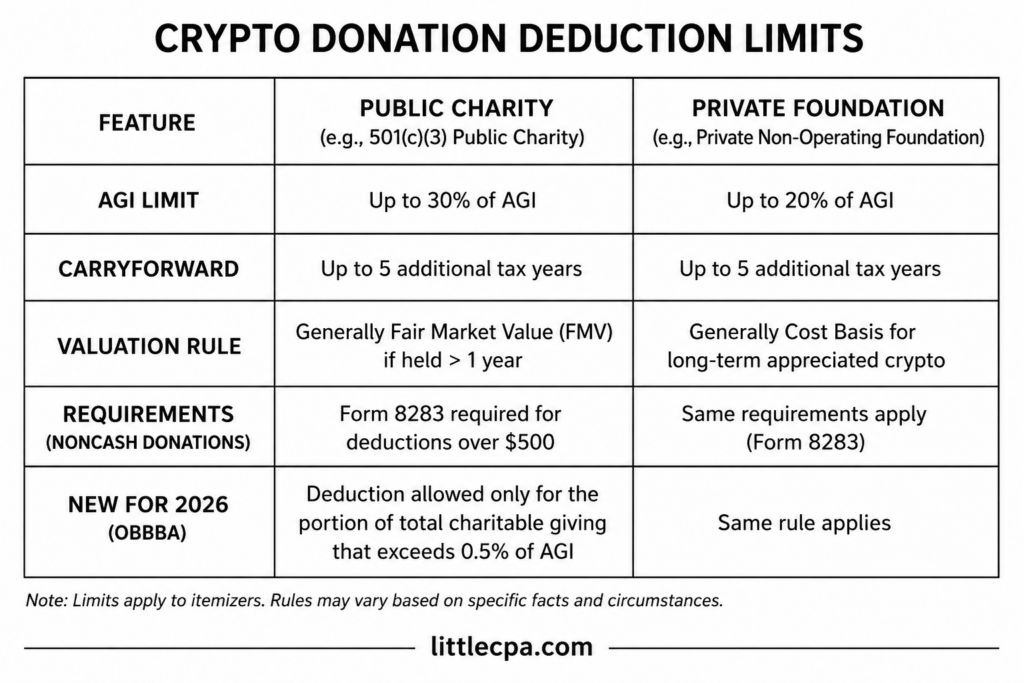

If you donate cryptocurrency held for more than one year to a qualified public charity, your deduction is generally limited to 30% of your Adjusted Gross Income (AGI). Amounts exceeding the limit may typically be carried forward for up to five additional tax years.

Note: Donations to certain private foundations – which are typically charitable organizations funded and controlled by an individual, family, or corporation rather than broad public support – may be subject to lower deduction limits and different tax rules.

So, the tax treatment can vary depending on the organization and how the gift is handled.

New for 2026: Beginning in 2026, the “One Big Beautiful Bill Act” added a new limitation for taxpayers who itemize deductions. Under the law, charitable contributions are deductible only to the extent that your total annual giving exceeds 0.5% of your AGI.

For example, if your AGI is $200,000, the first $1,000 of otherwise deductible charitable contributions generally will not produce a tax deduction. This new floor applies in addition to the existing AGI percentage limitations.

2. Confirming “Qualified Organizations”

To receive a deduction, you must give to a qualified organization, such as a church, private foundation or a 501(c)(3) public charity. Political organizations and most private individuals do not count.

To confirm an organization’s tax-exempt status, you can visit the IRS Tax-Exempt Organization Search.

Additionally, you will always want the charity’s development or fundraising associate to check the charity’s Gift Acceptance Policy. Some nonprofits are not yet equipped to handle digital assets or may require that all crypto be liquidated immediately upon receipt.

3. The Power of Donor-Advised Funds (DAFs)

If your favorite charity cannot accept cryptocurrency directly, a Donor-Advised Fund (DAF) can serve as an effective alternative.

A DAF is a charitable giving account sponsored by a public charity or financial institution. Instead of donating cryptocurrency to the end charity itself, you contribute the digital asset to the DAF, receive a potential immediate tax deduction, and then recommend grants to qualified charities over time.

This approach can simplify the administrative and tax complexities often associated with cryptocurrency gifts. Many DAF sponsors already have systems in place to receive, liquidate, and document digital asset donations, which can reduce compliance concerns for both the donor and the nonprofit organization.

DAFs can also provide flexibility for donors who want to contribute cryptocurrency during a high-income year but distribute charitable grants gradually in future years.

Note: Not every DAF sponsor accepts every type of cryptocurrency, and some may immediately sell the donated asset upon receipt rather than continue holding it, so it is important to confirm their policies before initiating the transfer.

4. Holding Periods and Valuation

Timing is everything in tax planning, especially with cryptocurrency donations. How long you have held the asset before donating it can significantly change both the size of your deduction and the taxes you avoid.

→ Related: Cryptocurrency Taxes: Your Top Questions Answered

Long-Term Holdings (Held More Than 1 Year)

If you donate cryptocurrency that you have held for more than one yea to a qualified pubic charity, you can generally deduct the asset’s Fair Market Value on the date of the donation, assuming the gift is made to a qualified public charity.

For highly appreciated assets, this can create a double tax benefit:

- A charitable deduction based on the current market value

- No tax owed on the unrealized gain

For example, if you purchased Bitcoin for $5,000 and it is worth $25,000 at the time of the donation, gifting the Bitcoin directly may allow you to deduct the full $25,000 while avoiding tax on the $20,000 gain.

Short-Term Holdings (Held 1 Year or Less):

If the cryptocurrency has been held for one year or less, the tax benefits are more limited. Your deduction to a qualified public charity is generally restricted to the lesser of:

- Your original cost basis, or

- The Fair Market Value at the time of the gift

This means appreciation that occurred during the short holding period usually does not increase your deduction.

Because cryptocurrency prices can fluctuate rapidly, documenting the value on the exact date and time of the donation is also critical. Keep records of wallet transfers, exchange values, receipts from the charity, and any supporting valuation documentation in case the IRS requests substantiation later.

5. Filing Form 8283 and Appraisals

Large crypto donations can require additional forms to be filed with your tax return. The IRS uses aggregate amounts for these thresholds:

- Over $500: You generally must file Form 8283, Section A for noncash charitable contributions exceeding $500.

- Over $5,000: You generally must obtain a qualified appraisal for donated cryptocurrency and complete Form 8283, Section B, which includes signatures from both the qualified appraiser and the receiving charity.

- Over $500,000: The same appraisal and Form 8283 requirements apply, but you must also attach the full qualified appraisal to your tax return.

Donating cryptocurrency comes with specific tax and reporting rules, but when structured properly, it can be one of the most tax-efficient ways to give. Planning ahead can help you maximize your charitable impact, reduce potential capital gains taxes, and avoid costly filing mistakes.