Investing in Index Funds

Nearly a quarter of all U.S. household financial assets are held in index funds. This upward trend continues into 2026 as more people recognize the long-term value of a “set it and forget it” strategy.

While no investment is entirely immune to loss, the historical performance and risk management of these funds put many conservative investors at ease.

→ Related: Investing 101: 5 Things Every Modern Investor Needs to Consider

Understanding the Core Definitions

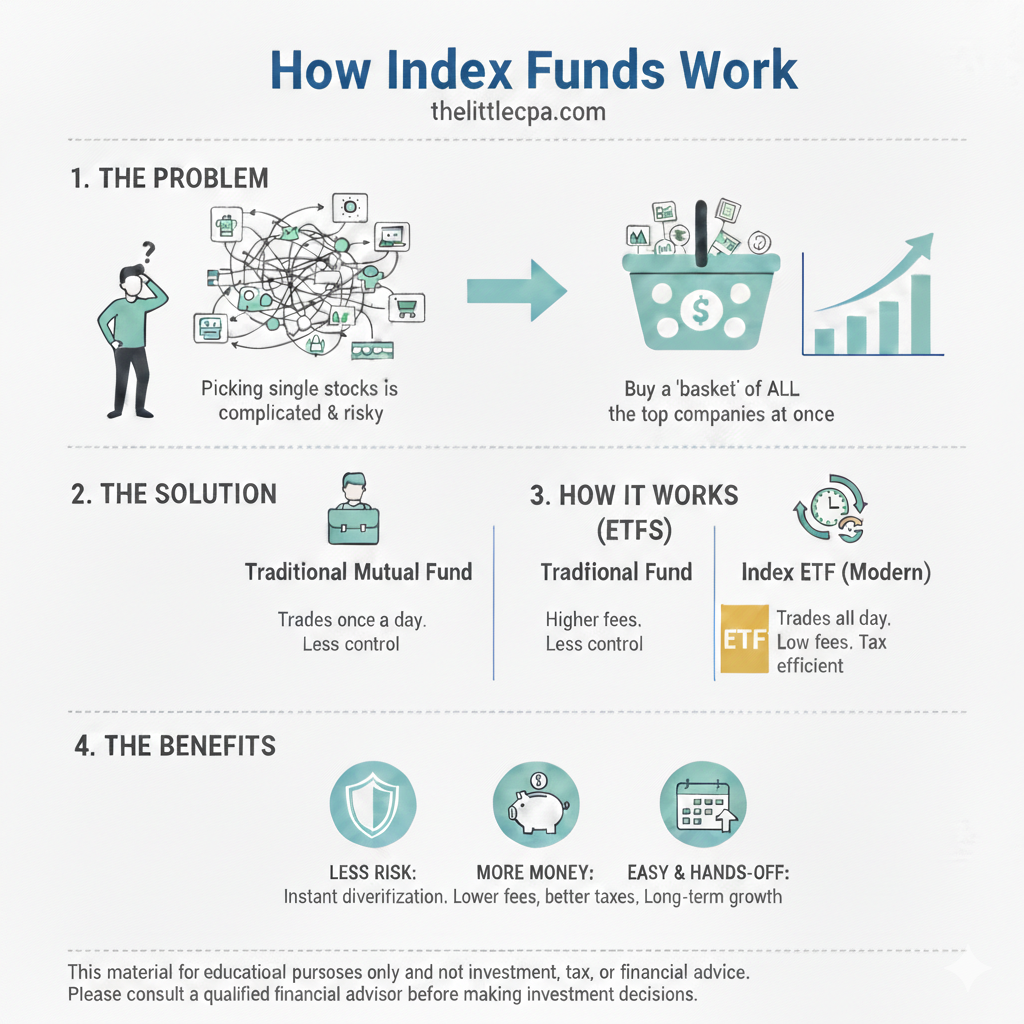

Before you dive into investing in index funds, you must understand a few fundamental terms.

- Market Index: This is a “basket” of securities that represents a specific sector of the market. Common examples include the S&P 500 (large companies), the Russell 2000 (small companies), and the Nasdaq (tech-heavy).

- Index Funds: As defined by the SEC, these funds seek to track the returns of a specific market index.

If a stock is like a single box of cereal, an index fund is like the entire cereal aisle. An index fund can be a mutual fund or an exchange traded fund (ETF).

Index Mutual Funds

Think of index mutual funds like a giant basket that can grow as big as needed. Every time someone wants to join, the fund simply creates a new spot for them.

A professional manager runs the fund and makes sure it holds a little bit of every company in a specific list (like the “Top 500 Companies”). Instead of trading with other people on a stock market apps, you buy and sell directly through the company that owns the fund.

Because of this, the price isn’t constantly jumping around. It is calculated just once a day after the markets close, so everyone who bought or sold that day gets the exact same price.

Capital Gains Tax

When you invest in a traditional mutual fund, the manager often has to sell stocks to raise cash whenever other investors decide to sell their shares. These sales can trigger “capital gains taxes” for everyone in the fund, meaning you might owe the IRS money even if you didn’t sell anything yourself.

Exchange Traded Funds (ETFs)

Think of a mutual fund like a movie ticket you can only buy or return at a set price after the theater closes for the night. An ETF is more like a concert ticket being traded on a site like StubHub, where the price changes every second and you can buy or sell it whenever you want while the show is running.

While they can track the same indexes as mutual funds, they offer several distinct advantages:

- Intraday Trading: Unlike mutual funds, ETF shares trade like individual stocks on an exchange. This means prices fluctuate throughout the day, allowing you to buy or sell at any moment during market hours. Frequent traders tend to prefer ETFs over index mutual funds.

- Tax Efficiency: ETFs use a unique “in-kind” exchange process that allows them to move stocks in and out without selling them for cash. Because the fund avoids selling assets on the open market, it doesn’t create those surprise tax bills for you, making it a much more tax-efficient way to grow your wealth.

Actively Managed Funds

Unlike index funds, actively managed funds employ a professional team to hand-pick stocks in an attempt to “beat the market.”

In an actively managed fund, a professional stock-picker (the “manager”) is constantly researching and trying to time the market to beat everyone else. In an index mutual fund, the manager has a much simpler job: they are basically on “autopilot,” instructed to match a specific list of companies (like the S&P 500) exactly.

To determine if the fund is index-based or actively managed, look at the “Management” section of the prospectus or the fund name; an index fund will explicitly name a benchmark it is “tracking” (like the S&P 500), whereas an active fund will state its goal is to “seek” or “outperform” the market through professional selection.