What can homeowners deduct on taxes? Homeowners can potentially deduct property taxes, mortgage interest, home office expenses, and exclude a large portion of their profit when selling their home. Homeowners under a certain income threshold can deduct up to $40,400 in State and Local Tax (SALT) payments.

- The SALT deduction cap increased dramatically in 2026 to $40,400 for most filers, meaning more homeowners will benefit from itemizing their deductions.

- Mortgage interest on loans up to $750,000 ($375,000 for married filing separately) remains deductible.

- The Section 121 exclusion lets you exclude up to $250,000 ($500,000 for married filing separately) in home sale profits from your taxable income if you’ve lived in the home for at least two of the last five years.

What Can Homeowners Deduct on Taxes?

Buying a home is one of the biggest financial decisions you’ll ever make. And while most people focus on building equity, there’s another benefit that often goes underutilized: homeowner tax deductions.

Whether you’re a first-time buyer or a longtime homeowner, understanding these four deductions could put real money back in your pocket.

1. Property Tax Deduction

Every homeowner pays property taxes.

Local governments use these taxes to fund roads, schools, public buildings, and other community programs. The amount you owe is typically based on your home’s current market value.

Property tax is a State and Local Tax (SALT) deduction, reported on Form 1040, Schedule A. If you itemize your deductions, you can deduct the property taxes you paid during the year.

The 2026 SALT Cap

Here’s where things get exciting. Under the original 2017 Tax Cuts and Jobs Act (TCJA), the combined SALT deduction, which includes property taxes and state income or sales taxes, was capped at $10,000. For homeowners in high-tax states like New York, New Jersey, and California, that cap stung.

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, raised that cap significantly:

- 2026 SALT cap: $40,400 (up from $10,000)

- Married filing separately: $20,200

- The cap increases by 1% annually through 2029, then reverts to $10,000 in 2030.

This is a temporary window, but a meaningful one. If your combined state income taxes and property taxes are between $10,000 and $40,400, you may now be able to deduct the full amount.

One important note for higher earners: The expanded SALT cap begins to phase out once your Modified Adjusted Gross Income (MAGI) exceeds $500,000 for joint filers ($250,000 for married filing separately). The benefit reduces by 30% of the excess above those thresholds, but all filers retain a minimum SALT deduction of $10,000.

2. Mortgage Interest Deduction

When you finance a home with a mortgage, your monthly payment includes two components:

- Principal — the amount you originally borrowed (not deductible)

- Interest — the cost of borrowing, paid at a fixed or variable rate (deductible)

The interest portion is often largest in the early years of your loan, which means if you buy a home mid-career, you could be capturing a valuable deduction during your highest-earning years.

→ Related: Is Interest on Home Equity Loans and HELOCs Tax-Deductible?

The Mortgage Acquisition Debt Limit

Mortgage interest is deductible on Form 1040, Schedule A if you itemize. Here are the current limits:

- Mortgages originated after December 15, 2017: Deductible interest on up to $750,000 of home acquisition debt ($375,000 for married filing separately)

- Mortgages originated on or before December 15, 2017: Deductible interest on up to $1,000,000 of home acquisition debt ($500,000 for married filing separately)

- For mortgages above these limits, the deductible interest is prorated

Good news: The OBBBA permanently extends the $750,000 limit, so there’s no more uncertainty about whether this provision will expire.

New in 2026: Private Mortgage Insurance (PMI) Is Now Deductible

Starting in tax year 2026, Private Mortgage Insurance (PMI) premiums are treated as deductible mortgage interest.

If you put down less than 20% when you bought your home, you’re likely paying PMI — and now you can deduct it. This is a win for many first-time buyers and those who purchased homes in expensive markets.

A quick reminder: don’t rack up mortgage debt just for the tax write-off. The deduction is valuable, but you still need to spend a dollar to save a fraction of one. The math only works in your favor when the mortgage makes financial sense on its own.

3. Home Office Deduction

If you use a dedicated part of your home for business, you may qualify for the home office deduction. And, this one applies to both homeowners and renters.

Do You Qualify?

The IRS requires you to meet two tests:

- Exclusive and regular use: You must use a specific area of your home exclusively and regularly for business. Think: a spare bedroom that’s set up as your office, used only for work.

- Principal place of business: Your home must be your primary place of business, or a place where you regularly and substantially conduct business even if you also work elsewhere.

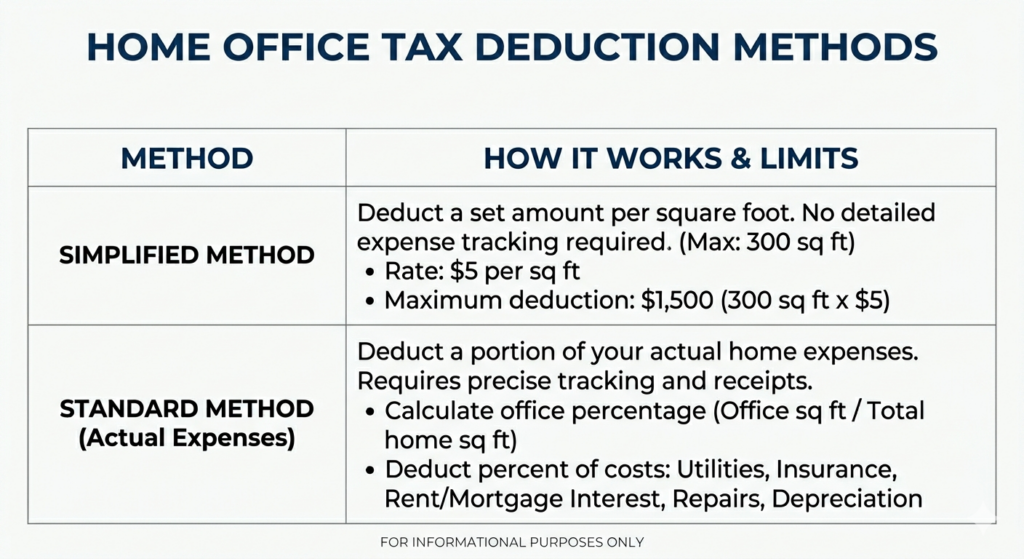

How to Calculate It

The home office deduction is calculated on Form 8829 and reported on Schedule C of your Form 1040. You have two options:

Depreciation Recapture

If you use the regular method and claim depreciation, that depreciation can affect your tax basis and may create depreciation recapture when you sell the home. Under the simplified method, depreciation is treated as zero, so it does not reduce your home’s basis.

A few nuances to keep in mind: the deduction is not available just because you sometimes work from home, and the IRS has specific rules for employees versus self-employed individuals. Also, some taxpayers may meet the qualification rules through a home space used for administrative or management activities, even if they perform some work elsewhere.

4. Home Sale Exclusion (Section 121)

This is arguably the most powerful tax benefit available to homeowners. Yet, it’s one that many people don’t fully appreciate until they’re ready to sell.

Under IRS Code Section 121, you can exclude a significant portion of your home sale profit from taxable income:

- Up to $250,000 for single filers

- Up to $500,000 for married couples filing jointly

How It Works: A Real Example

Say you and your spouse purchase a home for $400,000. You live there for three years. The home appreciates and sells for $900,000. Your realized gain is approximately $500,000 (before factoring in improvements made to the home, which can increase your cost basis and reduce your taxable gain).

Under Section 121, that entire $500,000 gain could be excluded from your taxable income. Zero federal income tax on a $500,000 profit.

Who Qualifies?

To claim the exclusion, you must have:

- Owned the home for at least two years out of the five years before the sale

- Used it as your primary residence for at least two years out of the five years before the sale

The two years don’t need to be consecutive. Keep careful records of when you moved in and out — the dates matter.

One caveat: If you claimed home office depreciation under the standard method, that depreciation will be recaptured and taxed when you sell, even if the rest of your gain is excluded. The exclusion limits also have not been adjusted for inflation since 1997, so in markets with dramatic appreciation, some sellers may still owe capital gains on any profit above the threshold.

Note for state filers:

Most states conform to the federal Section 121 exclusion, but a few do not. New Jersey, for example, does not recognize it. Always check your state’s rules.

Frequently Asked Questions

Q: Can I deduct property taxes if I don’t itemize?

No. Property taxes are an itemized deduction on Schedule A. If you take the standard deduction, you cannot separately deduct property taxes.

Q: Is mortgage interest deductible on a second home?

Yes. You can deduct mortgage interest on your primary residence and one second home (like a vacation home), as long as the combined acquisition debt stays within the $750,000 limit.

Q: Can renters claim the home office deduction?

Yes. The home office deduction is available to both homeowners and renters, as long as you meet the exclusive and regular use requirements.

Q: What happens if my home sale gain exceeds the Section 121 exclusion?

Any gain above the exclusion limit is taxed as a capital gain. For most homeowners, the long-term capital gains rate applies (0%, 15%, or 20% depending on your income). Any depreciation previously claimed is taxed at a maximum 25% rate.

Q: Does the new $40,400 SALT cap affect everyone equally?

No. The expanded cap phases out for taxpayers with MAGI above $500,000 (joint filers) or $250,000 (married filing separately). Very high earners may still be limited to $10,000. The phase-out reduces the cap by 30% of income above the threshold.

Q: Does the SALT cap change expire? Yes. Under current law, the $40,400 cap (with 1% annual increases) applies through 2029. In 2030, it is scheduled to revert to $10,000 unless Congress acts again.

Bottom Line: What Can Homeowners Deduct on Taxes?

Homeownership is multifaceted. When you’re deciding whether to rent or buy, taxes should be part of the equation. And if you’re already a homeowner, knowing what’s available, and staying current on changes like the expanded SALT cap and new PMI deduction, could make a real difference at tax filing time.

For some people, these deductions are a meaningful strategy for reducing tax liability and building long-term wealth. For others, the standard deduction still wins. Either way, knowing your options puts you in control.

Disclaimer

Please note that the financial advice and information presented on this blog are not personalized to your specific financial circumstances. This post is for informational purposes only and is not tax, legal, accounting, or investment advice. The Little CPA does not create a professional-client relationship by publishing this content. Please consult a qualified professional before making decisions based on this information. Any reliance you place on the information provided is strictly at your own risk.

Research and Verify

While every effort has been made to ensure the accuracy and reliability of the content, we do not make any representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability of the information. We strongly encourage our readers to conduct thorough research and verification independently.