Interview with Thomas Kopelman

Because many of his clients are in strong financial positions, Thomas Kopelman often suggests establishing a HELOC even without an immediate borrowing need. We spoke with him about the rationale, appropriate use cases, and key risks.

When Should You Open a HELOC?

The Little CPA: Thomas, you often recommend that homeowners open a HELOC even before they need it. What’s the thinking there?

Thomas Kopelman: “Oftentimes, a HELOC is best used as a backup emergency fund. The goal is not to use it to buy things you cannot afford, but to let it be there just in case you ever need it.”

The Little CPA: So what conditions make it the right time to open one?

Thomas Kopelman: “You pay interest based on how much you use. If you open one for $100K but don’t use it, you are not paying interest on it. It’s best to use when interest accrues at a fixed rate, in a low interest rate environment, when you have plenty of equity in the home, and when you’re in a strong financial position overall.”

In short, the best time to open a HELOC is before you desperately need one — when your finances are healthy enough that you probably won’t have to use it.

When Should You NOT Open a HELOC?

The Little CPA: Who should stay away from a HELOC?

Thomas Kopelman: “I would not recommend this for people who will have no income and no plan to pay this back. You typically want to be in a strong position — have cash on the sidelines, not have high-interest debt, etc.”

The Little CPA: What about using a HELOC to fund a new business?

Thomas Kopelman: “A HELOC for starting a business is less of a good idea than using cash. I would rather use cash and have the HELOC as a backup in case you needed it.”

Bottom Line: A HELOC is a tool for people with financial stability, not a lifeline for people who are already stretched thin.

How Do You Manage the Risks?

The Little CPA: What’s the biggest mistake you see people make with HELOCs?

Thomas Kopelman: “Way too many took these out with large balances, did big home projects, and now the interest rate is high and they cannot pay them down. You need to properly plan for repayment when the time comes. Make sure you have enough cash flow to actually pay the loan down.”

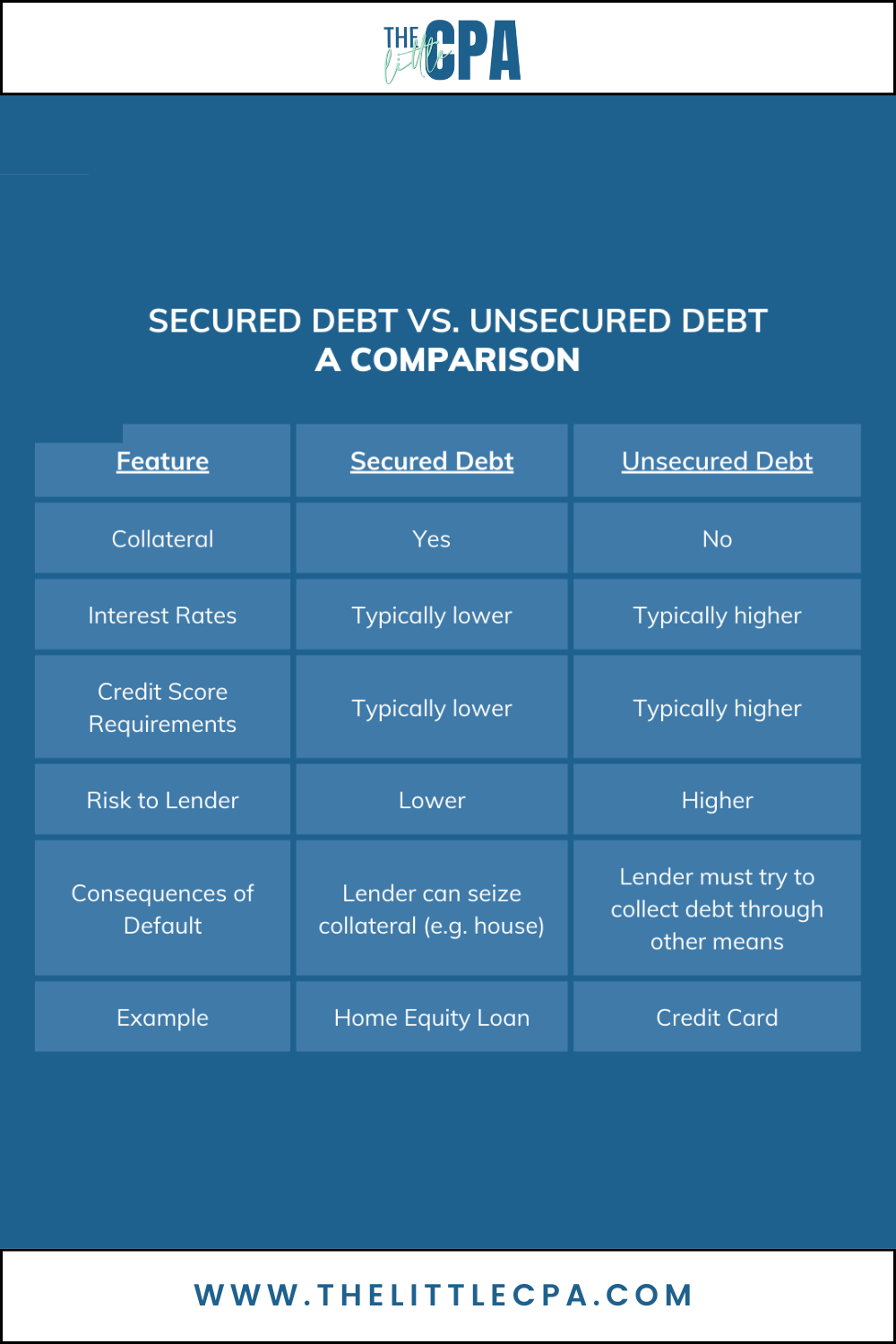

This is the core risk that doesn’t get enough attention. A HELOC is secured debt; your home is the collateral. If you can’t repay, you could lose it.

Understanding the difference matters:

– Secured debt is backed by an asset the lender can seize if you default (like your home or car).

– Unsecured debt has no collateral — think credit cards, personal loans, and student loans.

Does Debt Consolidation Into a HELOC Make Sense?

The Little CPA: Can you walk us through when consolidating debt into a HELOC actually makes sense?

Thomas Kopelman: “This can be a good strategy if someone has a bunch of high-interest debt like personal loans, credit cards, etc. Normally, consolidating all debt into a HELOC allows you to move your other debt into a way lower interest loan.”

The Little CPA: So what’s the tradeoff?

Using a HELOC to pay off unsecured debt reduces interest cost in many cases, but it converts that debt into an obligation secured by the home. This materially increases the potential downside if repayment becomes difficult. If life gets hard and you miss payments, the consequences are much more serious.

Debt consolidation using a HELOC is generally more appropriate when:

- There is a defined and realistic repayment plan.

- Income is stable and sufficient to support repayment.

- Home equity levels remain conservative after the new borrowing.

- Interest savings meaningfully exceed fees, rate risk, and closing costs.

How Is a HELOC Better Than a Credit Card or Personal Loan?

The Little CPA: In plain terms, why might a HELOC beat a credit card or personal loan?

Thomas Kopelman: “They can be way better than credit cards or personal loans just because the rates are normally lower. Though, I would not recommend someone use this for daily spending at all. It typically makes sense for funding housing projects or something along those lines.”

In general, HELOCs provide lower-cost borrowing due to being secured by real estate, but that same feature increases the consequences of nonpayment.

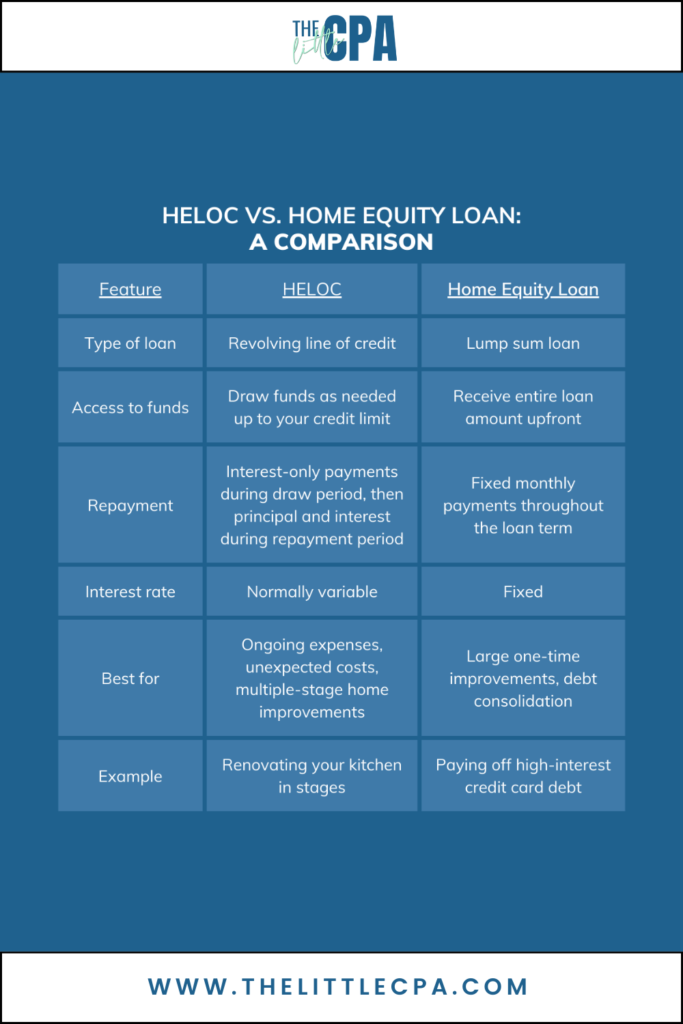

HELOC vs. Home Equity Loan: What’s the Difference?

A HELOC isn’t the only way to borrow against your home equity. A Home Equity Loan is a common alternative, and they work very differently.

Quick example:

Let’s say you have a one-time, predictable expense—like replacing your roof—and you know the total cost will be about $20,000. In that case, a home equity loan may be a better fit. You receive the funds as a lump sum, lock in a fixed interest rate, and repay it in equal monthly installments over a set term, which makes the cost easier to plan for.

Now consider a project like converting your garage into an apartment, where costs come in stages—permits, materials, labor—and the total may evolve over time. In that scenario, a HELOC may be more appropriate. You can draw funds as needed during the draw period rather than borrowing the full amount upfront. Because most HELOCs have variable interest rates and may allow interest-only payments initially, your monthly payments can change over time, especially once the repayment period begins.