The 529-to-Roth IRA Rollover Explained

Before 2024, you had two options with unused 529 funds 1) transfer the funds to another qualifying family member or 2) pull the money out and pay taxes plus a 10% penalty on the earnings.

Now there’s a third option: roll unused funds into a Roth Individual Retirement Account (IRA) for the 529’s beneficiary.

→ Related: Investing with a Roth IRA: Q&A with Bryan Hasling, CFP®

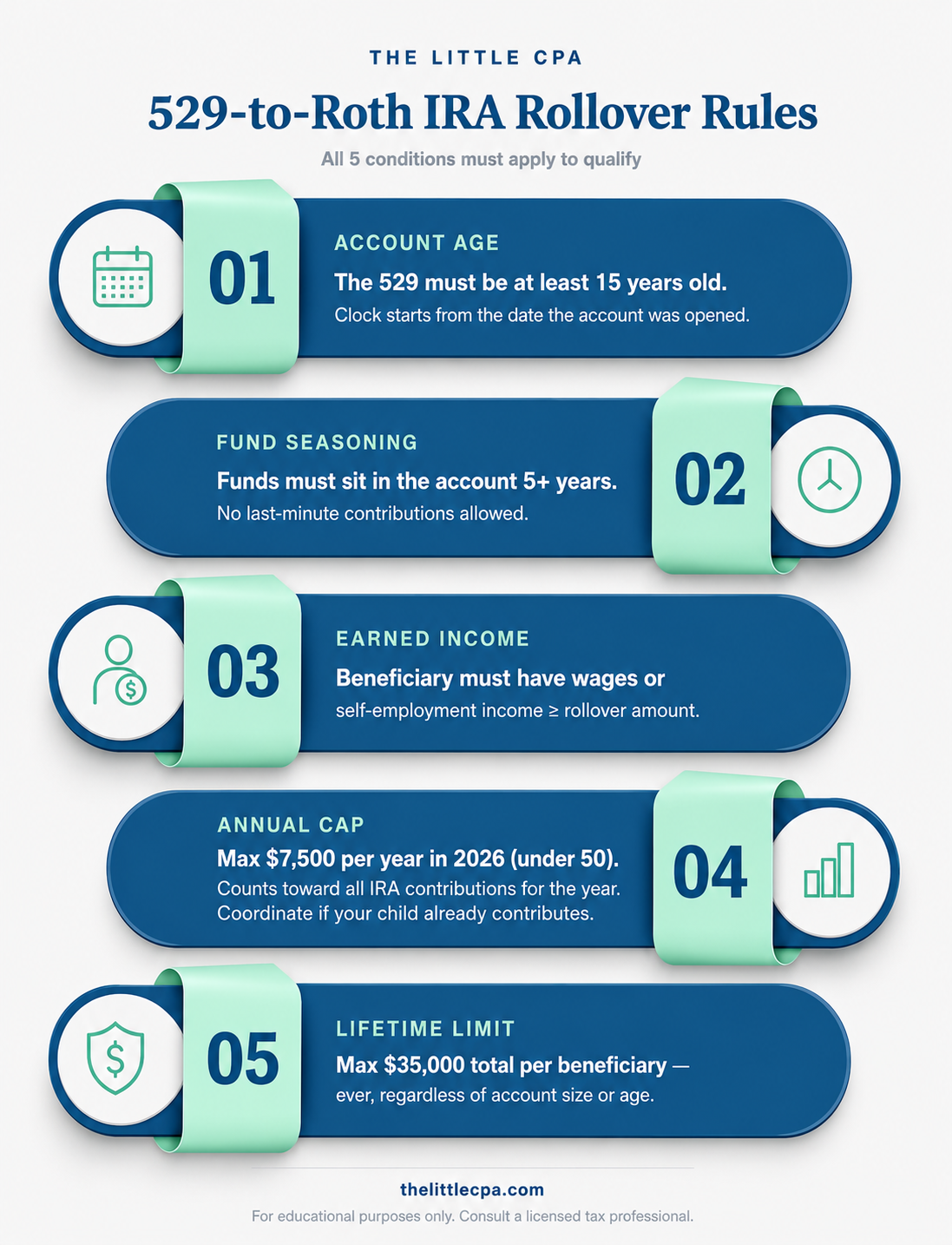

The Rules for a 529-to-Roth IRA Rollover

To qualify, all of the following must apply:

- The 529 account must be at least 15 years old. The clock starts from when the account was opened.

- The funds being rolled over must have been in the account for at least 5 years. You can’t make a last-minute contribution and immediately roll it to a Roth IRA.

- The beneficiary must have earned income. They need wages or self-employment income equal to or greater than the amount being rolled.

- Annual rollovers cannot exceed the IRA contribution limit. For 2026, that’s $7,500 for individuals under age 50. This limit applies across all IRA contributions for the year. So if your child already contributed $3,500 to a Roth IRA, only $4,000 more can come from the 529 rollover.

- Lifetime rollovers are capped at $35,000. Regardless of how long the account has been open or how much is in it, the maximum that can ever be rolled to a Roth IRA is $35,000 per beneficiary.

Why This Matters

Contributions grow tax-free and qualified withdrawals in retirement are also tax-free. Rolling unused 529 funds into a Roth IRA is essentially a way to convert education savings into a retirement head start, without penalties.

For families worried about “over-saving” in a 529, this rule is a game-changer.