- A Roth IRA allows your investments to grow tax-free, and qualified withdrawals in retirement are also tax-free.

- To take tax- and penalty-free withdrawals of earnings, you generally must be age 59½ and have satisfied the five-year rule. However, contributions (your original deposits) can be withdrawn at any time without taxes or penalties.

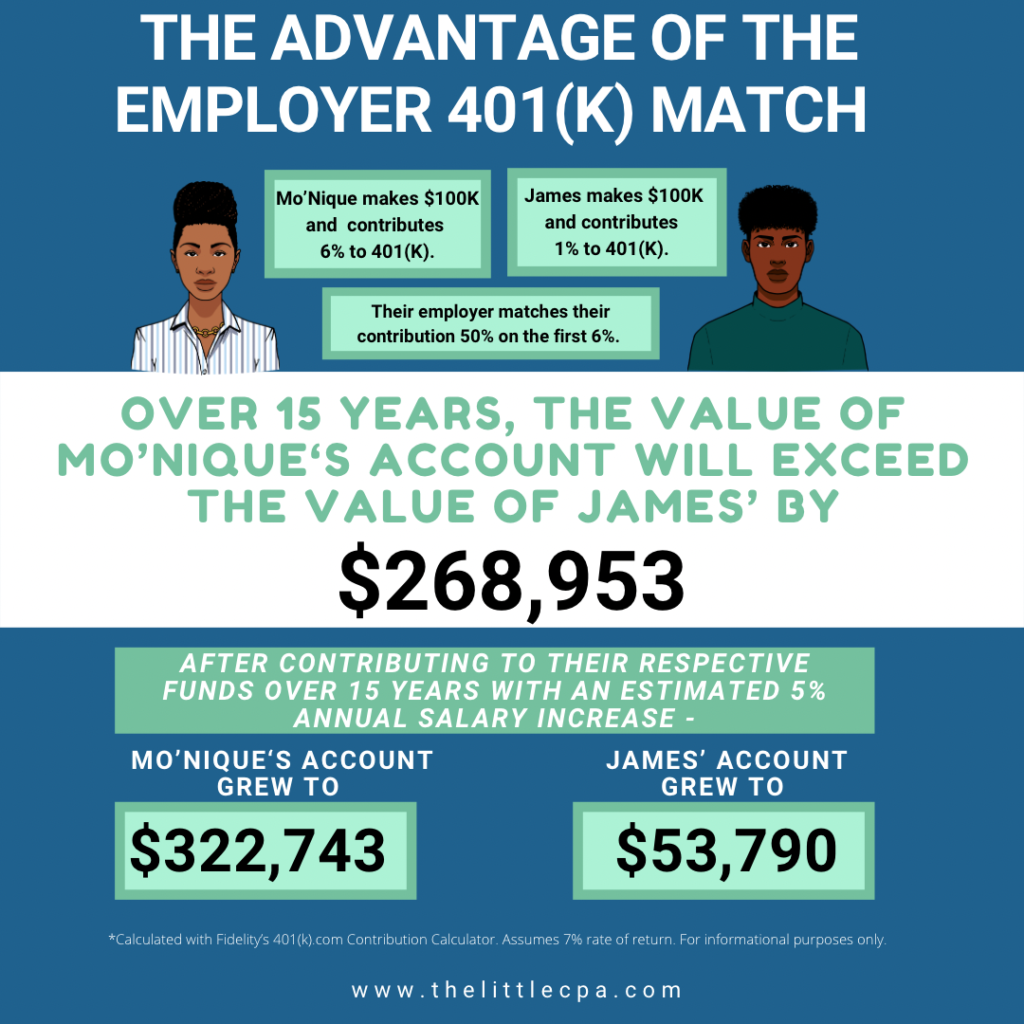

- It is often wise to capture your full employer 401(k) match before contributing to a Roth IRA, as the match provides an immediate return on your investment.

Updated February 1, 2026

Investing with a Roth IRA

A Roth IRA is a type of individual retirement account that allows your investments to grow tax-free.

Contributions are made with after-tax dollars, meaning you do not receive a tax deduction upfront. However, the trade-off can be substantial: qualified withdrawals, including earnings, are entirely tax-free in retirement.

Because of these advantages, the IRS imposes specific rules on eligibility and contribution limits. Understanding how these rules work is essential when determining whether a Roth IRA fits into your overall financial strategy.

To provide practical insight, The Little CPA spoke with Bryan Hasling, Certified Financial Planner, about how Roth IRAs function within a real-world financial plan.

How does a Roth IRA work?

Bryan: A Roth IRA is one of the most powerful investment accounts an investor can own. If done properly, all growth from your investments can be withdrawn completely tax-free in retirement.

There is no tax deduction upfront for saving into these accounts. The main benefit is the future tax-free growth.

To get the most benefit from the growth in your Roth IRA, you must meet 2 qualifications:

- your Roth IRA must be open for 5 years, and

- you must withdraw after age 59.5.

If you don’t reach those two, the growth portion of your withdrawal is subject to tax and 10% penalty.

You already paid tax. The IRS does not tax it again.

Contributions are always accessible regardless of account age

No annual tax drag while inside the account

Tax-free if qualified. Taxed and penalized if not.

Account must be open 5+ years and you must be age 59½ or older

There is an important exception to this tax and penalty: you are allowed to withdraw your contributions at any time, even if you withdraw before retirement years.

Since a Roth IRA’s tax-free benefit is so powerful, the IRS limits who can save into them and how much.

The Little CPA Note: For 2026, you can contribute up to $7,500 if you are under 50. If you are 50 or older, you can add an extra “catch-up” contribution of $1,100, bringing your total to $8,600.

→ Related: 529-to-Roth IRA Rollover: What You Need to Know

When Is the Best Time to Start a Roth IRA?

Bryan: At the highest level, you should save into Roth IRA if you’re ready to save more for your retirement goals.

Remember, the key benefit is that you can earn tax-free growth if you meet the requirements.

If you need cash in the next few years (or well-before age 59.5), there are likely better accounts to help you with those goals, instead of a Roth IRA.

→ Related: Investing 101: 5 Things Every Modern Investor Needs to Consider

As mentioned, you are allowed to withdraw your contributions portion (not the growth) before retirement years, without penalty. For that reason, many people use Roth IRAs for both short-term and long-term goals.

For instance, the contributions can serve as an added emergency fund if you are using the account for short-term goals.

In my experience, however, I generally suggest that you use a Roth IRA for pure, long-term savings. I find that it is much simpler to coordinate your overall finances when each account has a specific role in your plan.

But personal finances are… personal.

Each person should choose what feels best to them.

Should I contribute to a Roth IRA if I already have a 401(k)?

Bryan: If you are ready to begin saving for the long-term, usually the best place start is in your company’s 401(k) plan (if available). Like IRAs, 401(k)s are tax-advantaged retirement accounts, although the tax benefits and contribution rules differ.

I like 401(k)’s because the set-up is easier for new investors.

→ Related: The Roth feature within certain 401(k) plans

Even better, your company might incentivize you by offering an “employer match.”

This means that if you save into your account, they’ll follow your lead and deposit money in your account. This is as close to “free money” that you can get.

If you have an employer match, saving here should (almost always) be a top priority.

Once you’ve taken advantage of the employer match, you can then decide what other types of accounts you want to use to save and invest.

This is where it pays to know how all your accounts work.

The Roth feature within certain 401(k) plans

Bryan: For most 401(k)’s, the default savings option is pre-tax. Meaning, you can reduce your tax liability by contributing money into the account. But, you will pay taxes on future withdrawals.

These days, many 401(k) plans also offer a “Roth feature” which provides the same tax-free advantages that a Roth IRA offers.

The Little CPA Note: Starting in 2026: If you are 50 years and older and earned more than $150,000 last year and want to make “catch-up” contributions to your 401(k), the law now requires those specific contributions to be Roth-based (taxed at contribution, tax-free at withdrawal).

With a Roth 401(k), you might not need to open a separate Roth IRA until you’ve taken full advantage of your current 401(k) limits. The mechanics are much easier and the amount you can annually contribute into a 401(k) is higher than an IRA.

Once the Roth 401(k) is fully taken advantage of, you can start to look at a Roth IRA to supplement the savings.

The Little CPA Note: Keep in mind that, unlike the Roth IRA, a Roth 401(k) has a required minimum distribution after age 73. So, if you live beyond age 73, you will have to withdraw a portion of your 401(k) and thus cannot pass the full value of your account to a beneficiary.

| Roth 401(k) | Roth IRA | |

|---|---|---|

| Who opens it | Your employer sets it up; you opt in | You open it yourself at any brokerage |

| Eligibility | Anyone whose employer offers one — no income limit | Must have earned income; income limit applies — high earners may be phased out |

| Contribution limit | Much higher annual limit Check IRS.gov |

Lower annual limit; shared across all IRAs Check IRS.gov |

| Catch-up contributions | Available at age 50+; higher catch-up at age 60–63 | Available at age 50+ |

| Employer match | Yes — possible Employer may match; match funds land in pre-tax account |

No Individual account — no employer involvement |

| Tax treatment | Contributions after-tax; qualified withdrawals tax-free | Contributions after-tax; qualified withdrawals tax-free |

| Investment choices | Limited to your plan’s menu — typically mutual funds | Open universe — stocks, bonds, ETFs, mutual funds, etc. |

| Required minimum distributions | RMDs required Must start at age 73 (unless still employed) |

No RMDs No withdrawals required in your lifetime |

| Early withdrawal — contributions | Generally not accessible while still employed | Can withdraw contributions anytime, no tax or penalty |

| Early withdrawal — earnings | Tax + 10% penalty before age 59½ (exceptions apply) | Tax + 10% penalty before age 59½ (exceptions apply) |

| Loans | Often allowed Plan rules vary |

Not allowed |

| 5-year rule | Applies per plan; rolling to a Roth IRA inherits that IRA’s clock | Clock starts Jan 1 of the first year you contribute to any Roth IRA |

| Portability | Can roll over to a Roth IRA when you leave your employer | Stays with you regardless of employment |

| Backdoor option | Not applicable | High earners can contribute via backdoor conversion |

What type of assets can be held in a Roth IRA?

Bryan: You can invest in a wide range of publicly traded stocks, bonds, mutual funds, and ETFs in your Roth IRA. “Publicly traded” means the investment is listed on a public market and can be bought or sold through that market.

Investing in funds is a simple way to diversify your holdings and not need to worry about placing bets on specific companies.

The Little CPA Note: You can also purchase real estate and other non-traditional assets within a self-directed Roth IRA. Although the “tax-free” earnings from these sources of income seem appealing, keep in mind these types of Roth IRA holdings are subject to strict rules and tax compliance. Speak with a tax, financial and legal advisor before making this investment within your Roth IRA.

Investing with a Roth IRA: The Bottom Line

Roth IRAs offer plenty of benefits, and they’re worth looking into if you want to save for retirement.

But, Roth IRAs are not for everybody. In fact, if your income is over the IRS threshold, you might not be able to contribute to a Roth IRA unless you use the “backdoor.”

The Little CPA Note: High earners should watch the new income phase-outs. For 2026, the ability to contribute directly to a Roth IRA begins to phase out at $153,000 for single filers and $242,000 for married couples filing jointly. These taxpayers should discuss the pros and cons of using the backdoor strategy with a qualified tax and wealth management professional.

About the Expert: Bryan Hasling CFP®

Bryan helps folks plan for retirement and reach financial independence on their terms. He is a CFP® professional.

In addition to custom portfolio design, he helps clients navigate their finances around complex topics related to their company-stock (RSUs, ESPP) and options (ISOs, NQSOs).

In 2022, he was named to InvestmentNews’ 40 under 40 class, an honor given to the top thought-leaders in the industry

Disclaimer: This material is for informational purposes only and is not intended as tax, legal, or accounting advice. Consult your own advisors before making significant financial commitments.

No Professional Advice (Investment, Tax, or Legal) The content provided by The Little CPA is for informational and educational purposes only. The Little CPA does not offer investment, tax, legal, or any other type of professional financial advice. None of the information on this website constitutes a recommendation, solicitation, or offer to buy or sell any securities or financial instruments. While we discuss financial concepts and strategies, these are general in nature and do not take into account your specific objectives, financial situation, or needs.

No Professional-Client Relationship Your use of this website or engagement with this content does not create a CPA-client, attorney-client, or financial advisor-client relationship. The Little CPA is not your fiduciary. A professional relationship is only established through a formal, signed engagement letter specifically tailored to your individual circumstances. You should consult with a qualified professional who is familiar with your unique financial situation before making any significant financial or legal decisions.

General Information Only This material is prepared by The Little CPA as a resource for self-research and general education. While we strive for accuracy, the rapidly changing nature of tax laws and financial regulations means this information may not be complete or applicable to your specific situation. We disclaim all liability for any actions you take based on the information found here.

Past Performance & Risks Any examples of tax savings or investment returns are for illustrative purposes only. Past performance does not guarantee future results. All financial decisions carry inherent risk, and the user assumes all responsibility for any losses or outcomes resulting from their personal financial choices.

Third-Party Risk References to specific software, banks, financial professionals, or storage providers are not endorsements. We are not liable for any issues, data breaches, or financial losses that may arise from your engagement with third-party vendors.